CSDS POLICY BRIEF • 12/2026

By Daniel Fiott

30.4.2026

Key issues

- The EDF has become a stable and widely used instrument for EU defence cooperation.

- France, Italy, Germany and Spain dominate EDF participation, but smaller states are increasingly active.

- Russia’s war against Ukraine has accelerated EDF investment in combat and defence capability innovation.

Introduction

On 15 April 2026, the European Commission released the results of the 2025 call under the European Defence Fund (EDF). Overall, in 2025, the Commission invested some €1.07 billion in 57 defence projects, which demonstrates the continued popularity and relevance of the EU-level funding tool. The Commission reports as part of its rollout of the 2025 EDF projects that some 634 unique legal entities from 26 member states and Norway and Ukraine are part of projects that will feed into critical defence domains such as artificial intelligence (AI), cyber, sensors, drones and flagship areas such as air and missile defence, space and (counter-)drones. From 2021 to 2027, the European Union (EU) will invest €7.3 billion in defence research and development (R&D) under the Fund.

In this respect, the 2025 results constitute a sufficient period – five years – to make preliminary observations on the functioning of the Fund. In this CSDS Policy Brief, we will first look at the 2025 results using publicly available data provided by the EU, before then comparing the results across five years since 2021. We are interested in examining where EDF financial support is being channelled, which innovators coordinate projects and which member states participate in EDF projects. We also give some indication of the diversity of innovators that participate in the Fund.

The 2025 EDF call results

Under the 2025 EDF call, 57 specific projects were successful, and this embodies further evidence of the Fund’s ability to bring together defence firms, innovators, researchers and consultants into European R&D projects. Given Russia’s continued war on Ukraine and dramatic shifts in the transatlantic relationship, the EDF, often perceived as too small in financial scale and overly technical in nature, has nevertheless emerged as proof that European defence can be built upon tangible cooperation between Europe’s primes, mid-caps, SMEs and research institutes. While it is legitimate to ask whether the EDF has delivered tangible results, we should be careful with the assumption that Fund projects need to deliver a physical result in the form of weaponry, components or technologies. Indeed, the Fund is also about the software of defence cooperation, including ideas and processes that push the innovation frontier in defence in Europe.

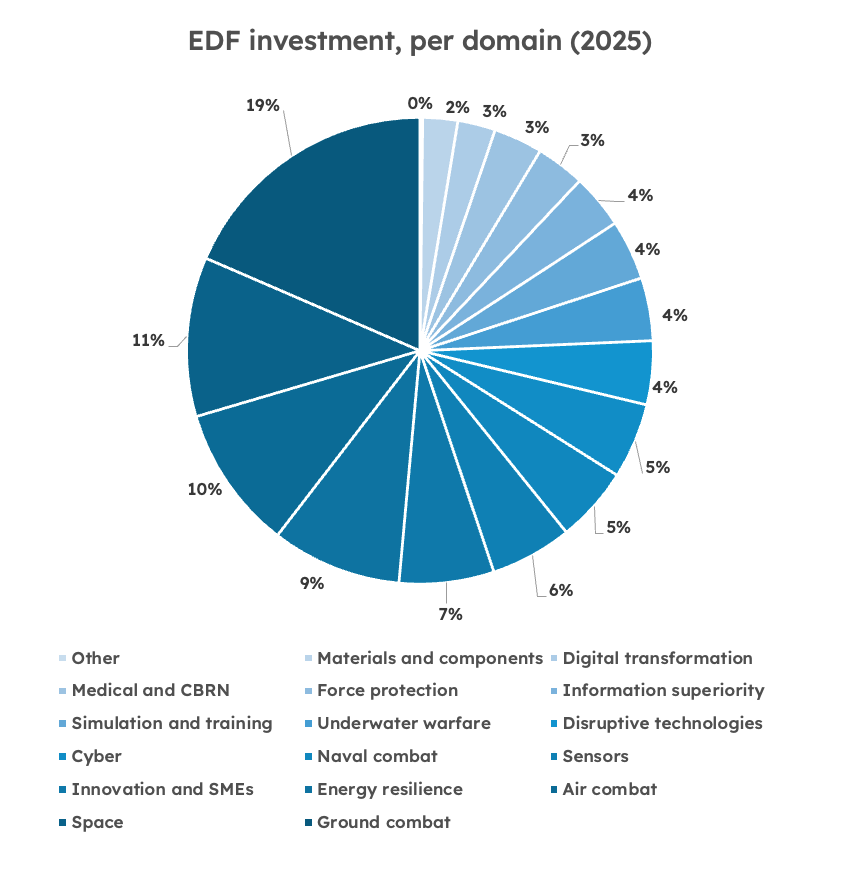

In 2025, the 57 specific projects fall across 16 different defence technology domains, including: 1) innovation and SMEs; 2) disruptive technologies; 3) simulation and training; 4) underwater warfare; 5) naval combat; 6) force protection and utility; 7) ground combat; 8) air combat; 9) materials and components; 10) energy resilience; 11) digital transformation; 12) space; 13) cyber; 14) sensors; 15) information superiority; 16) medical and CBRN. The bulk of investment under the EDF in 2025 has been channelled to ground combat (€191 million), space (€114 million), air combat (€103 million), energy resilience (€93 million), innovation and SMEs (€68 million), sensors (€59 million), naval combat (€54 million), cyber (€54 million), disruptive technologies (€46 million), underwater warfare (€45 million), simulation and training (€43 million), information superiority (€39 million), force protection (€35 million), medical and CBRN (€35 million), digital transformation (€27 million), materials and components (€25 million) and other.

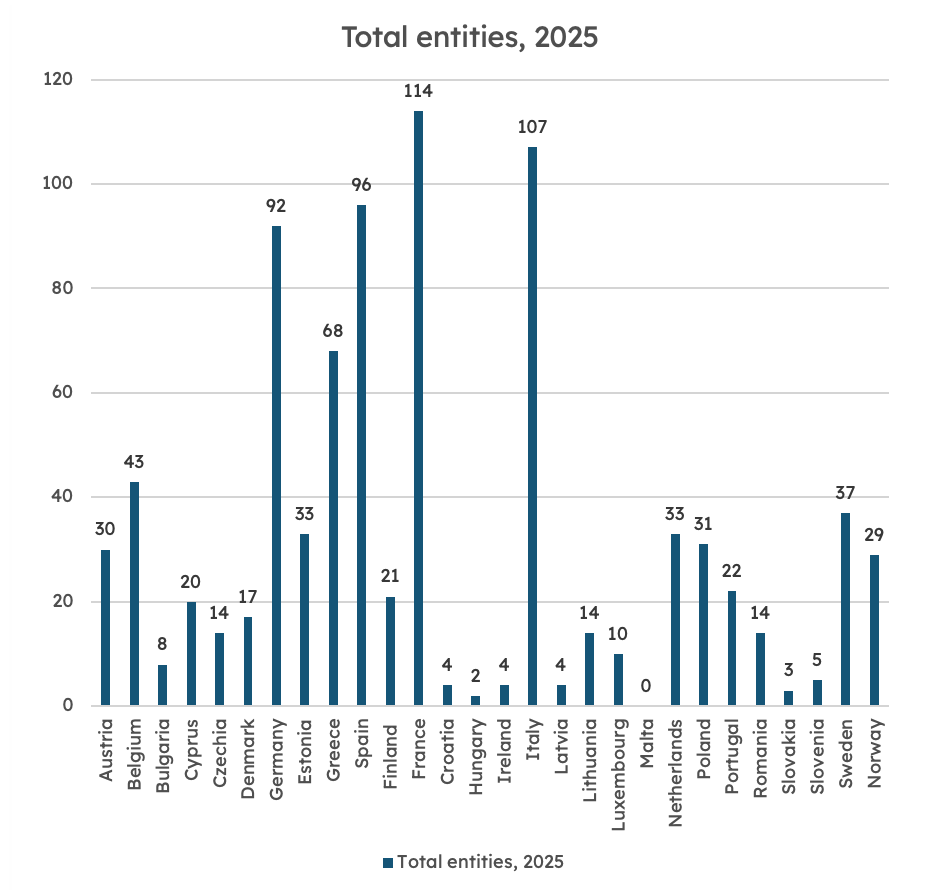

As part of the latest EDF results, firms and innovators from all EU member states and Norway, except Malta, were part of projects. As we can see, France is home to the most entities (114) participating in EDF projects, followed by Italy (107), Spain (96), Germany (92), Greece (68), Belgium (43), Sweden (37) and more. It is noteworthy that Norway, even though not a member of the EU, has 29 entities involved in EDF projects in 2025, taking it above the participation rate of 16 EU member states (only Portugal, with 22 entities, is close to Norway’s level of participation). The data shows that, in 2025, much like previous years, the main defence industrial players in the European defence market are indispensable for the management and motion of EDF projects, and smaller defence markets have only a relatively small participation level.

However, there are exceptions to this assertion. Indeed, we can see Belgium has a larger participation rate (at 43 entities) compared to Poland (31) and even Sweden (37). The same is true, perhaps even more so, for Cyprus. It is one of the Union’s smallest member states, but it has 20 entities involved in EDF projects in 2025, which is extraordinary given the size of its defence market. Cyprus performs comparatively well compared to say Finland (21 entities), Denmark (17) and Portugal (22). We do, however, have to be careful with such estimations as variations between member states are not only an expression of the motivation of innovators to bid for EDF projects, but also commercial decisions on whether it is worthwhile collaborating with partners through EU-sponsored projects. Indeed, many innovators are engaged in extra-EU commercial partnerships, or they rely more structurally on investment opportunities from national governments. In this sense, they may decide not to engage with EDF projects in the first place.

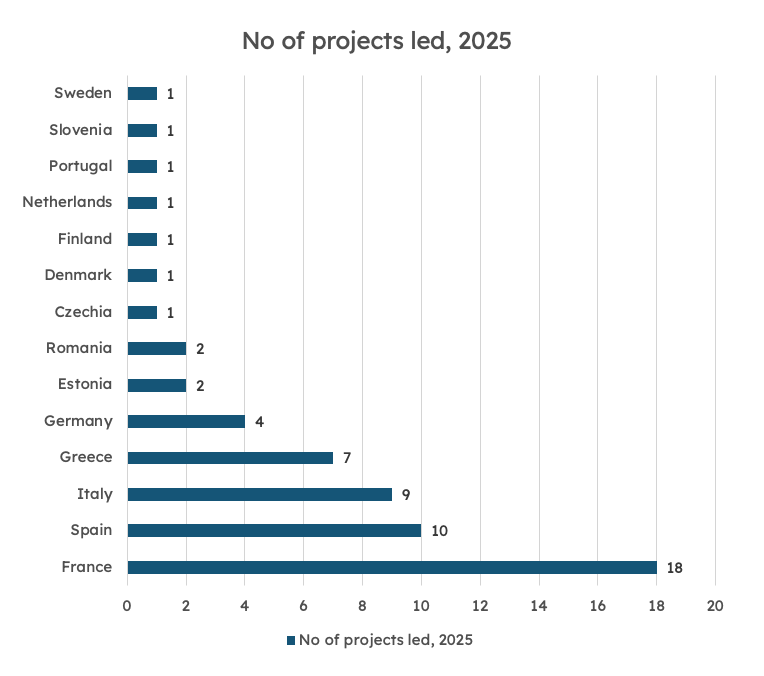

Every EDF project is organised among partners in the EU, but each project has a coordinator or lead. In reality, these coordinators are responsible for the overall management of the project, and they are, in most cases, the actors who devise the original concept of innovation behind the bid. In 2025, France was project lead for 18 EDF projects, followed by Sapin (10), Italy (9), Greece (7), Germany (4), Estonia (2), Romania (2), Czechia (1), Denmark (1), Finland (1), Netherlands (1), Portugal (1), Slovenia (1) and Sweden (1). Again, the data provides a few outliers with smaller EU member states, such as Estonia and Slovenia, managing EDF projects, with larger member states, such as Germany, only managing a handful of projects compared to the larger defence actors.

Participation in EDF Projects in 2025

| Entity |

Country |

Total No. |

| Thales |

France |

20 |

| Indra Sistemas |

Spain |

15 |

| Leonardo |

Italy |

15 |

| Austrian Institute of Technology |

Austria |

13 |

| Fraunhofer |

Germany |

12 |

| Saab |

Sweden |

11 |

| Safran |

France |

10 |

| TNO |

Netherlands |

9 |

| CAFA Tech |

Estonia |

8 |

| French Alternative Energies and Atomic Energy Commission |

France |

8 |

| Kongsberg |

Norway |

8 |

| Integrated Systems Development |

Greece |

7 |

| STAM |

Italy |

7 |

| Elettronica |

Italy |

6 |

| Centre for Research and Technology Hellas |

Greece |

6 |

| GMV Aerospace and Defence |

Spain |

6 |

| Netherlands Aerospace Centre |

Netherlands |

6 |

| Sener Aerospacial |

Spain |

6 |

| Airbus France |

France |

5 |

| Airbus space and defence |

Germany |

5 |

| Akmon |

Greece |

5 |

| Defsecintel Solutions |

Estonia |

5 |

| Signalgenerix Limited |

Cyprus |

5 |

| SINTEF |

Norway |

5 |

| Thales |

Italy |

5 |

| Swedish Defence Research Agency |

Sweden |

5 |

The 2025 EDF results also show that participation in projects is not necessarily concentrated in the hands of only a few entities. In other words, some member states reflect a diffuse form of participation, with several innovators and firms participating in projects, and many of these entities may not have previously applied for EDF support. For example, for Belgium, there is no concentration of participation with several entities participating in the 2025 projects. In Belgium, the only entity present in more than two EDF projects is Thales Belgium (with a maximum of 4 projects). Compare this with Austria, where there is also a good spread of entities across EDF projects, but where the Austrian Institute of Technology is involved in 13 projects in 2025. We can see above a list of participation of entities, per country, in 2025, where these entities are present in five or more EDF projects.

The evolution of the EDF, 2021-2025

When we study the various calls under the EDF since 2021, it is possible to create a rudimentary picture of how the Fund is operating in practice. Overall, the past five years have seen the Fund grow in popularity in the EU, which is also partly a function of word of mouth, European defence fairs, EDF info days, public engagement, national promotion and more. More European firms and innovators are aware of the purpose and nature of the EDF in 2025. Indeed, the 2026 call for proposals has already been published by the Union, with 10 calls worth some €1 billion. This 2026 call will focus on bids related to endo-atmospheric interceptors, a main battle tank, a multiple rocket launcher and a semi-autonomous vessel, in addition to critical technologies and support to SMEs. The evolution of investment in the EDF from 2021 to 2025 reflects an annual investment of approximately €1 billion in EDF projects.

Below are the details of how the EU has divided the yearly work programme investment. We can observe that the EU has invested €5.2 billion across five calls for proposals, whereby the Union has financed 282 projects involving 3,171 unique entities in the EU and Norway. Except for 2022, an average of 60 projects has been financed per year, and the resulting number of unique entities that participate in EDF projects has been stable at about 600 unique entities. In this sense, the data reveals the EDF’s consistent appeal in Europe, and it has managed to attract a critical mass of entities to support the projects. What the data fails to reveal at present, however, is how successful each EDF project has been, and it is not possible to gauge the status of each project presently. In time, one hopes that the European Commission is open and transparent with these results, so that we may gauge the level of output from the Fund.

Total EDF investment, 2021-2025

| Year |

Total Investment |

No. of Projects |

No. of Unique Entities |

| 2025 |

€ 1.07 billion |

57 |

634 |

| 2024 |

€ 910 million |

62 |

625 |

| 2023 |

€ 1.2 billion |

61 |

670 |

| 2022 |

€ 832 million |

41 |

550 |

| 2021 |

€ 1.2 billion |

61 |

692 |

| Total |

€ 5.2 billion |

282 |

3,171 |

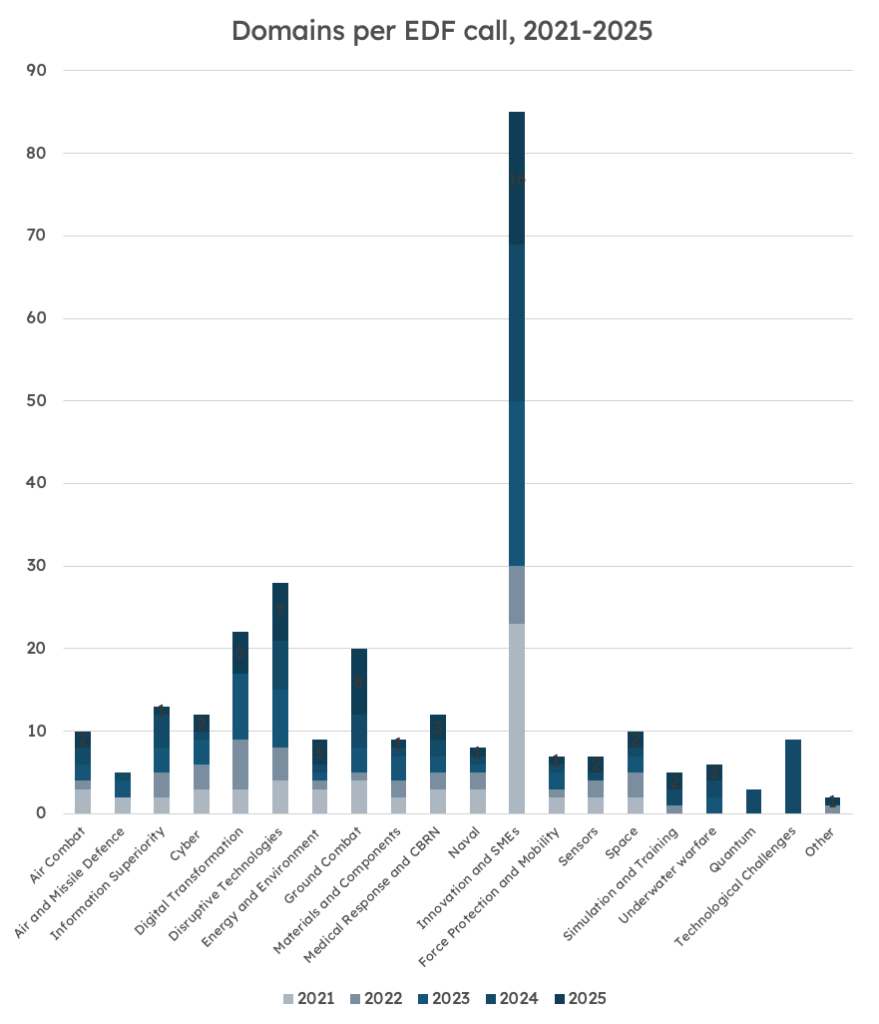

The data made available by the European Commission also helps us to look at trends over the past five years, since 2021, and to discern how the Fund has evolved. What we observe is that the “innovation and SMEs” domains represent the bulk of EDF projects from 2021 to 2025 (with 85 total projects), which is in keeping with the political and industrial objectives of the Fund. However, what is unclear from this rather broad heading is what exactly is classified as innovation, and it is unclear from the available data whether innovation refers mainly to weapons systems or the underlying software of a capability. This is the same for the categories of “Digital Transformation” and “Technological Challenges”. Where the categories are clear, we can see that there has been a consistent investment in cyber (12), ground combat (20), medical response and CBRN (12), information superiority (13), space (10) and air combat (10 projects).

What we learn about project variation across the past five EDF calls is also noteworthy. We observe consistent investment in all of EDF-sponsored domains, with only underwater warfare, quantum and air and missile defence becoming more important since Russia’s invasion of Ukraine. In fact, the Union has maintained steady investment across most domains, and only in a few instances can we say that the war in Ukraine has fundamentally altered the investment pattern. For example, before the 2022 war began, there were no underwater warfare projects, but after the war, six were initiated. In ground combat, five projects were financed before the 2022 war started, but from 2023 to 2025, this increased to 15 projects.

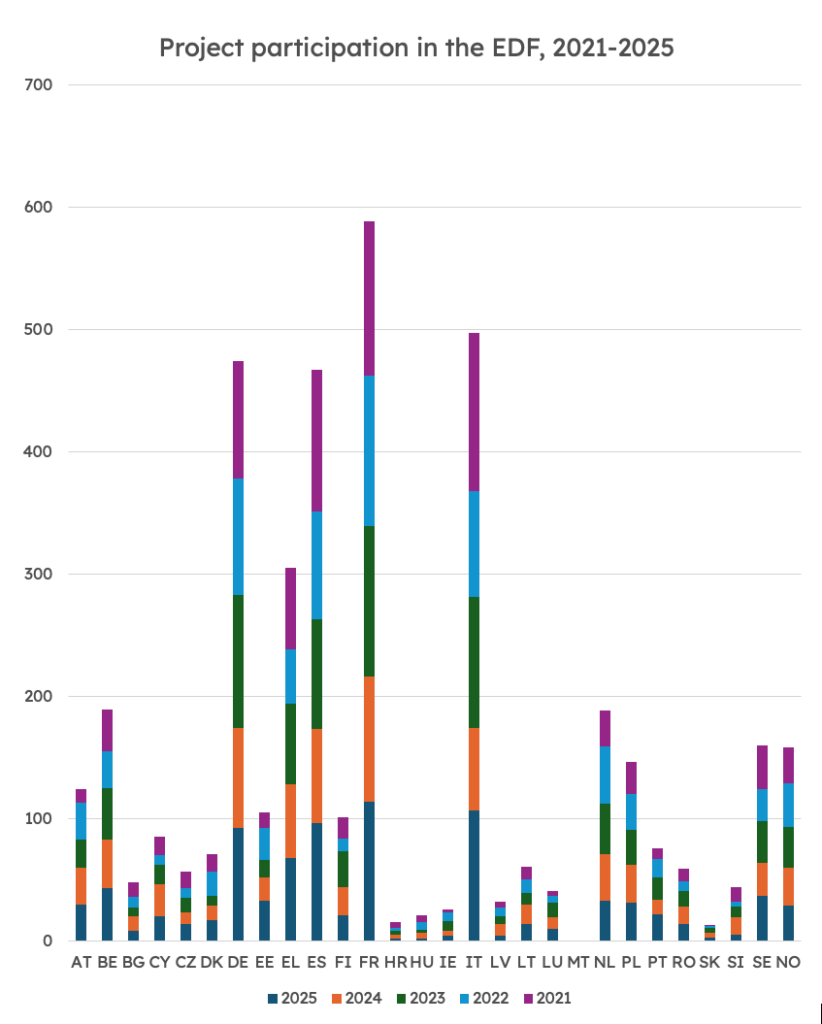

Over the past five years, we have also seen a relatively consistent pattern of project leadership in EDF projects. As we can see, France (588 total entities), Italy (497 total entities), Germany (474 total entities) and Spain (467 total entities) have dominated EDF project participation from 2021 to 2025. Those with the lowest participation rate over the past five years include Malta (0), Slovakia (13), Croatia (15), Hungary (21) and Ireland (26). What we learn from studying the data for trends is that Austria, Belgium, Cyprus, Estonia, Luxembourg, Poland and Romania are the member states that have consistently increased their participation in the EDF, on a year-on-year basis. Most member states and Norway maintain a relatively consistent level of participation across the five years of calls.

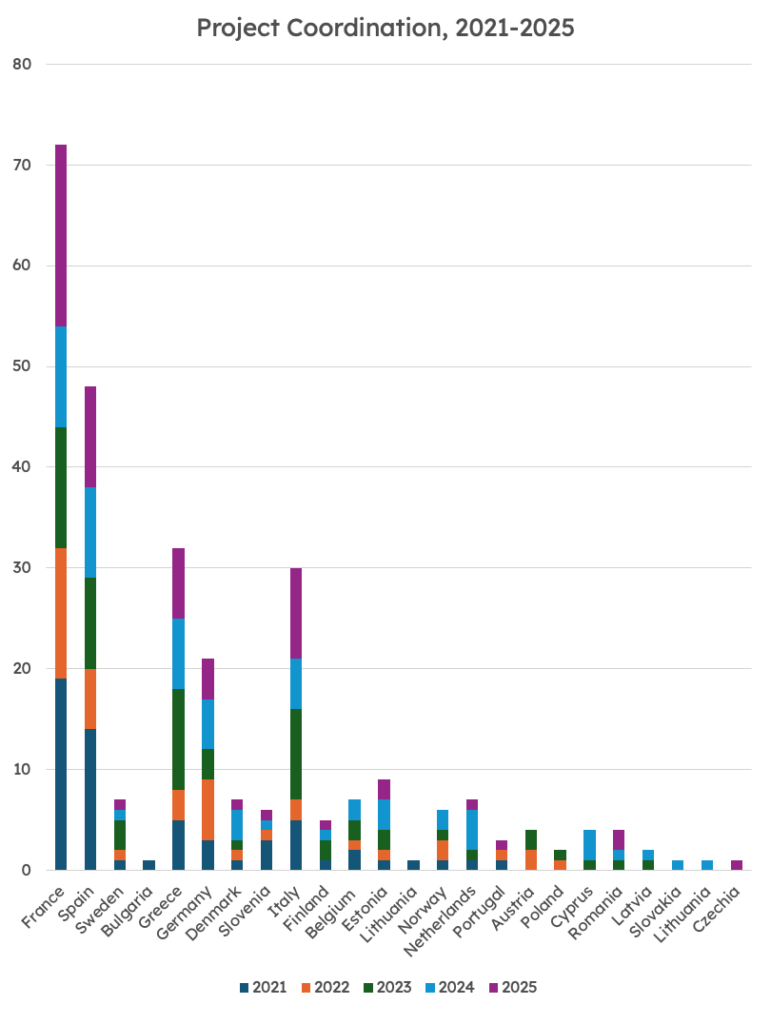

In terms of project coordination, the data reveals that France leads in the most projects since 2021 (72 projects), followed by Spain (48 projects), Greece (32 projects), Italy (30 projects) and Germany (21 projects). Yet, the data also reveals that smaller and medium member states have been able to lead EDF projects, and some have actually managed EDF projects relatively consistently since 2021. The stand-out project coordinators in this regard are Cyprus (4) and Estonia (9), which have comparatively smaller defence industrial bases.

Finally, we can also look in more detail at the entities that are most prevalent in EDF projects. As the table shows, many of these firms and innovators are perhaps obvious participants, but there is nevertheless an interesting mix of different entities involved in EDF projects since 2021.

Participation in EDF project, 2021-2025

| Entity |

Country |

TOTAL |

| Thales |

FR |

105 |

| Leonardo |

IT |

75 |

| Indra Sistemas |

ES |

68 |

| Fraunhofer |

DE |

60 |

| Saab |

SE |

53 |

| TNO |

NL |

50 |

| Austrian Institute of Technology |

AT |

47 |

| Safran |

FR |

45 |

| Rheinmetall |

DE |

40 |

| Commissariat a l Energie Atomique et Aux Energies Alternatives |

FR |

32 |

| Elettronica |

IT |

32 |

| Baltijos Pazangiu Technologiju Institutas |

LT |

30 |

| Airbus Defence and Space |

DE |

30 |

| Office National d’Etudes et de Recherches Aerospatiales |

FR |

28 |

| GMV Aerospace and Defence SA |

ES |

27 |

| Kongsberg Defence & Aerospace |

NO |

26 |

| Forsvarets Forskninginstitutt |

NO |

25 |

| Totalforsvarets Forskningsinstitut |

SE |

24 |

| Hensoldt |

DE |

24 |

| STAM |

IT |

23 |

| ISD Lyseis Olokriromenon Systimatonanonymos |

EL |

23 |

| Cafa Tech OU |

EE |

22 |

| Naval Group |

FR |

22 |

| Airbus |

FR |

22 |

| Stichting Koninklijk Nederlands Lucht – en Ruimtevaartcentrum |

NL |

21 |

| Sener Aeroespacial |

ES |

21 |

Conclusion: “funding failure”?

The first five years of the EDF in action demonstrate that the EU has succeeded in establishing a genuinely European framework for collaborative defence R&D. Despite criticisms over the Fund’s limited financial scale, the EDF has helped to create a nascent ecosystem linking Europe’s defence primes, SMEs, research institutes and innovators. The data reveals not only the centrality of established industrial powers, but also the growing participation of other, smaller member states. In this sense, the EDF is contributing to a gradual Europeanisation of defence innovation and industrial cooperation at a moment when Russia’s war against Ukraine and uncertainty in the transatlantic relationship have reinforced the strategic necessity of greater European defence readiness. The Fund appears to be adapting to the changing character of warfare and Europe’s evolving capability requirements.

However, while the Fund has proven its value as a catalyst for cooperation, its overall budget remains modest when measured against the scale of Europe’s capability shortfalls, industrial fragmentation and geopolitical pressures. The next Multiannual Financial Framework (MFF) will therefore represent a political test for the Union. If the EU is serious about defence readiness, technological sovereignty and industrial resilience, substantially greater investment under the EDF will be required. This means not only expanding the financial envelope of the Fund, but also ensuring continuity between collaborative research, capability development and procurement at the European level. Beyond money, however, it is necessary to shift Europe’s innovation mindset, which is still held back by risk aversion and a “bean-counting” mentality that seeks to avoid funding failure. In R&D, ingenuity should not be held back by these principles and “funding failure” still contributes to Europe’s innovation base.

__________

The views expressed in this publication are solely those of the author and do not necessarily reflect the views of the Centre for Security, Diplomacy and Strategy (CSDS) or the Vrije Universiteit Brussel (VUB). Image credit: Canva, 2026

ISSN (online): 2983-466X